A Discussion of Precious Metals as Money

By Hugo Salinas Price

www.plata.com.mxPresented at the Cheviot Sound Money Conference, January 27th, 2011, Guildhall, London

Elements for monetizing the silver ounce in British Pounds

In 2001 we elaborated the text for a Congressional Bill which would establish the method for monetizing the “Libertad” silver ounce in Mexico. Today, the idea of silver money is well known among Mexicans and we believe it is only a matter of time for this Bill to be approved. It is presently awaiting a vote in the Congress.

However, this project can also be carried out in any other country; all it requires is for that country to mint its own silver ounce and follow the fundamental outline which we have proposed for the Mexican silver ounce.

The Treasury is the entity that could and should monetize the silver ounce for the UK.

For the British Treasury the monetization of a silver coin would constitute an important source of income, since all of Europe – indeed the whole world - would wish to possess this coin of supreme quality. We must underline that the emission of this coin and its sale to the public implies no risk at all nor future responsibility for the issuer. Gresham’s Law, working in reverse, guarantees this: good money never seeks to exchange itself for bad money.

Such a coin of superior quality incorporates within itself its own reserve in the form of a silver content which represents the greater part of its monetary value. Issuing this coin does not mean that the pound ceases to be the currency of the UK. The monetized silver ounce becomes a part of currency in circulation, in parallel with paper and digital pounds.

This measure should not be regarded as a move to a “silver standard”.

Once the design of the silver ounce has been approved and the coin has been minted it will be given a quoted monetary value by the Treasury.

We must state at this point that the effective monetization of the silver ounce requires as an indispensable condition: that it shall not bear an engraved monetary value. We shall explain the reason for this condition, further on.

The Treasury quote will attribute a monetary value in pounds to the ounce. The quote will serve the same function which an engraved value gave to silver currency in former times.

This quoted monetary value will be superior to the intrinsic value; that is to say, to the value of silver in bullion form.

This margin of difference between the value of silver bullion and its quoted monetary value in coin form will cover the cost of minting and also grant the issuer a profit from seignorage. The size of the margin is optional; a modest margin is preferable to a large margin in order to avoid sporadic large increases in the monetary value of the ounce.

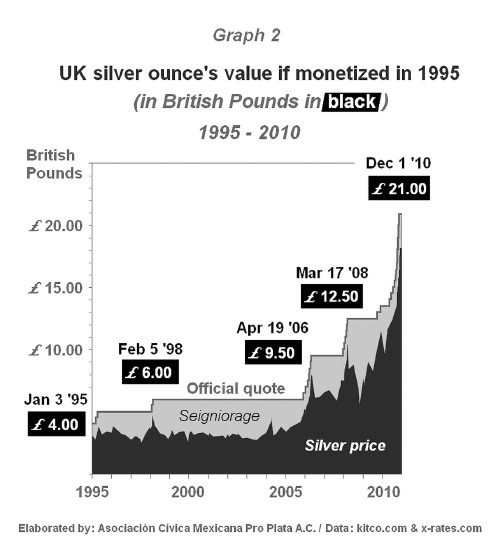

Let us take an example in order to illustrate the method for monetization.

On December 1st, 2010, the following prices were registered (for purposes of this exposition all prices are those registered on that day):

Spot silver: $28.74 dollars per Troy ounce (31.1 grams)

Dollar/British Pound: 0.639

The spot price of silver in British Pounds on that day was therefore:

$28.74 dollars per ounce x 0.639 = £18.36.

Let us add to this value, 50 pence (suggested) to cover cost of minting =

£18.36 + .50 = £18.86

By way of seignorage, let us add a base percentage of 10% over the cost:

£18.86 x 1.1 = £20.74

It will be impractical for owners of these ounces to use and remember this figure £20.74 in transactions in which they might wish to use this coin. Therefore, its monetary value will be rounded up to the next higher figure which will be a multiple of 50 pence. Thus, the monetary value would be determined as £21.00.

The rounding up is useful because it allows a greater margin for the operations of the issuer. Small and transitory rises in the value of silver will not require a new quote. The next quote, higher than £21.00 will be £21.50.

A new quote is imperative when the price of the silver ounce, plus its cost of minting, plus a 10% profit surpasses £21.00. In the previous example, the gross seignorage of the issuer was £2.14 (£21.00 minus £18.36 for the cost of silver), which represents a seignorage of 12.6% of the monetized price.

Let us suppose the cost of minting remains 50 pence; we can determine what price of silver will call for a new quote: £21.01 = (cost of silver ounce + 50 pence for minting costs) x 1.1 Solving the equation, we see that silver bullion would have to be £18.60/oz.

As long as the price of the Troy ounce of silver bullion fluctuates between £18.36 and £18.59, there will be no need to issue a new monetary quote for the ounce: it will remain at £21.00. The additional margin provided by the rounding-up of the monetary value protects the seignorage of the issuer.

Our example shows that the method of determining a monetary value for the silver ounce is quite simple and can be easily modified according to the actual cost of minting and according to the seignorage which may be considered desirable; the multiple to be used for ‘rounding up’ is also optional.

Now we come to the most controversial point regarding this measure:

What happens when the price of silver falls?

The answer is surprisingly simple: nothing happens.

The second indispensable condition for successfully carrying out the conversion of the silver ounce into currency which will circulate in parallel with the British pound is: the last monetary quote given to the ounce by the issuer must not be reducible. The reason for this unusual condition is that ever since silver ceased to have monetary value according to weight, the monetary value of all silver coins was always and everywhere a fixed value; it was a fixed value because all these silver coins bore an engraved or stamped value.

In order for the silver ounce to cease being a commodity and be currency it is indispensable that its nominal monetary value be a fixed value which cannot be reduced – just as is the condition of present British pound coins and bank notes – along with which the ounce is to circulate in parallel.

If the quote is allowed to fluctuate in value downward, according to the price of silver, then the ounce will not be currency: it will continue existing as a commodity.

Once the silver ounce becomes currency, thanks to the quote of the issuer, it ceases to be a commodity. Its monetary value, as is the case with current British pound coins and bank notes, is then independent of the material of which it is made; its monetary value must be just as constant: its quote must not be reducible Even if silver’s price were to fall to the value of copper – and we cannot visualize a worse case – the monetized silver coin would continue to be currency at whatever was the last quote. If a paper can be worth £100, surely a silver coin can represent the quote given to it by the issuer, independently of the value of the silver it contains.

Besides, even if we assume a very large fall in the price of silver, a silver coin with a monetary value in British pounds (which may be high with respect to the value of the silver in the coin) will always be preferable, in the public’s regard, to a British pound banknote which has no value content at all, being as it is, only a piece of paper.

As a historic proof of what we affirm, we present a graph which shows the history of the intrinsic value of a Mexican silver coin which was known as the “Peso 0.720”. This coin contained 12 grams of pure silver and as you can see in the graph, the value of silver bullion during the period from 1920 to 1945 fluctuated between 45 centavos of Mexican peso, down as far as 32 centavos in the Depression years of the 30’s.

As we can see in figure above, disappearance of this coin was not caused by falls in the price of silver; it was a rise in the price of silver which began in 1945 which caused the disappearance: its engraved or stamped value could not be altered to reflect the higher price of silver.

This is why the silver ounce which is to be monetized must not show an engraved monetary value.

All the silver coinage that existed in the world before World War II had an engraved value. Monetary inflation was created in all monetary systems during and after the war, and new industrial uses were found for silver; together, these factors caused a rise in the world price of silver. It became uneconomic to continue minting silver coins and in one country after another they disappeared from circulation; their silver content was worth more than their engraved monetary value. The public gathered up existing coins and the greater part of the silver coinage went to refineries, since silver bullion was worth more than the monetary value of the coins to be melted, whose monetary value could not be altered.

Global monetary inflation is a phenomenon whose end is not in sight. The monetization of the silver ounce will require its constant revaluation which will be possible because it will not have an engraved monetary value. This periodic revaluation will allow the monetized silver ounce to remain in circulation permanently.

In passing, we should mention that at present some silver coins are being minted with engraved monetary values far below their real value. This deliberately demonetizes them because it does not permit them to be used as currency. They continue to be a commodity subject to speculation.

The same perverse motivation is apparent in the case of silver coins whose monetary value is higher than their intrinsic value. In this case, the use of these coins as currency is sabotaged by minting only very small quantities and offering them to the public as simple numismatic curiosities. The French Mint played this frivolous game recently; it issued a tiny quantity of silver coins denominated in euros, to be sold to the public at prices far higher than their nominal value.

Therefore:

The coin must not bear an engraved nominal value in order to

allow the Treasury to raise its value to reflect the increase in

the international value of silver, thus ensuring that the coin will

remain in circulation permanently.

The quote must not be reducible so that the quoted silver ounce may function as any other coin in circulation.

In the case of Mexico, the Bill for the Monetization of the Silver Ounce contains two additional provisos:

1. The issuer will observe the silver market and detect possible speculative phenomena which may appear in that market. In order to prevent temporary speculative excesses from impacting the monetary value of silver, the Bank of Mexico will have a margin of six months to verify whether a large and sudden increase in the value of silver is a market phenomenon or a speculative disorder. During this period, it may suspend a new quote. This delay will have a minimal effect upon the monetary use of the silver ounce since the population will retain these coins in the expectation of new, higher quote, in not more than six month’s time. During the period in which the Bank of Mexico may delay the issue of a new quote in order to verify that the rise in the price of silver is a market phenomenon, there may appear transitory speculative premiums on the value of the monetized silver ounce; these will disappear as soon as a new quote is issued.

2. The issuer shall respond to the demand for this coin on the part of the public, by minting coins sufficient to cover such demand. Otherwise, the market will give this coin a speculative premium, above the issuer’s quote. The presence of premiums announces that the coin is losing its function as currency in exchange for a numismatic or speculative interest.

Spot silver closing price, plus cost of minting (estimated at 50 pence), times 1.1 for (suggested) 10% seigniorage, rounded up to nearest multiple (suggested) of 50 pence.

Saving is a dynamic phenomenon. The desire to save is practically innate in the human being but the capacity to save at any given moment is limited by the nature of things. Similarly, the public wishes to save – and quite especially it will wish to save silver coins – but its capacity to save is limited at any given moment. The issuer will recognize that a momentary limit to savings in silver has arrived when the public is using silver coins in daily transactions and deposits them in the banks for credit to bank accounts. The banks, who cannot effect transmissions of silver by electronic means, will perhaps find they have an excess of silver coins and return them to the issuer just as they do with British pound bank notes and coins.

This will be a signal that for the moment, the emission of silver ounces has exceeded the savings capacity of the public. The minting program may be modified to take this into account. The issuer will retain in its vaults, the minted silver that for the moment exceeds the demands of the public, with the certainty that the public’s demand will shortly present itself once again. It will never be forced to retain minted silver permanently because Gresham’s Law guarantees it: the public will always prefer to save a coin of superior quality as a part of personal and family savings.

Such are the main elements regarding the monetization of the silver ounce. Lastly, we should point out two things:

a. That a one-ounce coin might be too big a coin, given the rising price of silver. The same method of monetization could be carried out with a half-ounce or a quarter-ounce coin, which would allow more people to acquire silver coins for savings.

b. That to make the coins more durable, the content of pure silver - one ounce, half-ounce or quarter-ounce - of the selected coin should be alloyed to some degree with copper. (In the case of Mexico the coin to be monetized is one ounce of pure silver, because the population already owns a significant number of these coins.)

Minting silver without a silver mining industry

We have been proposing the monetization of silver, in such a manner that it will circulate permanently in parallel with fiat money.

We have reviewed our proposal from time to time – nine years is plenty of time to think – not in order to modify our proposal but to polish it.

Our latest musings on the subject of monetizing silver have to do with a question that has been put to us now and then: How may a country that has no silver mines monetize a silver coin?

Let us suppose the British Treasury decides to monetize a silver coin and grant it a monetary value in British pounds.

The British Treasury is facing hard times. The UK has a trade deficit and the idea of purchasing foreign silver which will be handed over to the public in exchange for fiat money does not appear to the Treasury as an urgent need; even if it wished to monetize silver, the Treasury simply could not afford it.

Under the “Open Mint” policy the US Treasury accepted all silver bullion for minting, for the account of the miners. Through 1872, all silver was potentially money. The US miners were digging up money, so to speak, and simply handing it over to the US Treasury for minting into silver dollar coins, for their own account. The newly minted silver coins belonged to the miners. This system was abandoned in 1873.

We propose a “Conditioned Mint” system of silver coinage as a route by which an Open Mint might be re-established eventually.

Under the “Conditioned Mint” system which we imagine, the British Treasury would announce its intention to purchase and mint a certain amount of bullion silver, on a first come first serve basis, at the market price prevailing on the date of purchase, for its own account. The sellers of silver would have to agree to receive, in payment of their silver, minted silver coins with a monetary value in British pounds equal to the price of the sale. The system we outline has three conditions:

a. The amount to be minted is determined, from time to time, by the Treasury.

b. The silver is purchased by the Treasury and minted for the account of the Treasury, and not for the account of the providers of the silver.

c. The silver purchase is paid to the sellers in monetized silver coins with a monetary value in British pounds equal to the purchase price.

The reasons for the conditions are as follows:

a. The Treasury is essaying a new system. It will wish to be cautious. This condition allows the Treasury to try the waters with purchases under its control. If everything goes well, as we believe it will, the Treasury may expand its activity and decide to accept all silver presented to it for minting. But until the system proves itself the Treasury has the option of continuing or not continuing to purchase silver. The “Open Mint” policy is approached gradually – in our opinion, the only possible way it can be reinstated eventually.

b. The Treasury purchases the silver bullion for its own account because there is a special form of payment involved. (See point “c”)

c. Sellers who present their silver to the Treasury must agree to receive, in payment, the monetary value of their bullion silver in monetized silver coins.

Here is an example of an operation where the Treasury has announced it will purchase up to 100 tonnes of silver bullion on such and such a date, at market price. (For purposes of this example, the market price will be the closing price of silver on December 1, 2010.)

100 tonnes of silver = 3,215,074 Troy ounces x £18.36/oz = £59,028,759 purchase price.

£59,028,759 are paid to the sellers of the silver in silver coins with a monetary value equal to that amount. The quoted monetary value of the silver ounce, as determined by our suggested factors for monetization, for the silver bullion price on December 1, 2010, would be £ 21.00. (We refer to our proposed method for monetizing a silver coin, to circulate permanently in parallel with fiat money, which can be read in English in the previous section of this brochure, or at www.plata.com.mx)

If the monetized silver ounce is quoted by the Treasury at £21.00, how many ounces would be required to pay those who sold 100 tonnes of silver to the Treasury? The payment of £59,028,759 by the Treasury would be effected by delivery of 2,810,893 monetized silver coins (59,028,759 / 21.00 = 2,810,893 monetized silver ounces)

Under our proposal to monetize a silver coin, the monetized coins have a monetary value superior to the bullion value of the silver contained in the silver coins. An estimate of the difference, given the previous conditions, reveals that the monetary value of 100 tonnes of silver bullion would be approximately 12.6% lower than the monetary value of 100 tonnes (3,215,074) monetized silver ounce coins.

In effect, the sellers of silver to the Treasury would be losing about 12.6% of their silver in the operation. They would be obtaining the full price of their silver in British pounds, but they would receive in return only 87.4% of the silver sold. That 87.4% would take the form of monetized silver coins.

The difference of 12.6% of the purchased silver would be retained by the Treasury as its seigniorage or profit from the operation of minting the silver coins and monetizing them.

Here lies an opportunity for considerable profit for the Treasury, because the potential for expanding this activity is great. The Treasury would retain in its vaults 404,181 monetized silver ounces.

Would the sellers of silver be willing to sell their silver under these terms? We think that silver producers would be eager to accept Treasury offers to purchase silver on these terms, for the following reasons:

If the sellers sell silver to the US Treasury for minting into silver coins, they receive fiat money – in digital form – in payment. Under the system we propose, the sellers receive silver money – real money – in payment of their silver. They get full payment in British pounds, but in the form of real money. We think the alternative is quite attractive.

The sellers can deposit these monetized coins in British banks at their monetary value; the banks can offer them to a public which will be eager to obtain them in return for payments in cash or with a charge to bank accounts. The demand for the coins will be enormous.

The coins, monetized in British pounds, are immune to devaluation; they can only rise in value, together with the underlying price of silver; they cannot fall in value, as silver bullion does from time to time, and they are immune to problems of bank solvency.

In time, the increasing availability of monetized silver coins will make it possible to offer international payments with the monetized silver coins. Foreign markets will accept these coins unquestioningly; indeed they will avidly seek these coins, because, as we have said, they are immune to devaluation of the British pound, they can only rise in monetary value as silver rises in price, and they are of superior quality as money. They are real money which exists independently of any banking system, which makes them immune to crises in the British banking system, or any other banking system, for that matter.

At present, banking crises threaten to wipe out entirely, at one stroke, all money on deposit in banking systems. The great world financial crisis shows no signs of abating; on the contrary, it is increasing in severity and a national banking default may cause a domino effect on world banking orders of magnitude worse than experienced in the 30’s. Banking systems have their governments by the throat and can demand, and obtain, bailouts to be paid by the taxpayers. Silver money in permanent circulation is the only available, practicable route to begin to free governments from the impositions demanded under duress by banking systems. A reform of the world’s monetary system which reinstates gold as the international numeraire is indispensable, but as things are at present, no one has any idea how this reform might be accomplished.

The demand for the British pound, reborn as a monetized silver coin circulating alongside its bastard brother the fiat British pound, will be worldwide. Every coin minted and sent abroad – and there will be tens of millions of them - will provide the Treasury with approximately 12.6% of its value, left behind as silver in the Treasury vaults.

The monetized silver ounce, used in international payments, achieves settlement of international debt: payment in silver extinguishes debt. Payment in fiat money does not and cannot extinguish debt. Therefore, silver ounces will be used as Reserves by Central Banks and stored in their vaults.

The demand for the monetized British silver ounce will drastically affect the market for silver, causing the price of silver to rise to unsuspected heights. This is all well and good, and no cause for concern. The higher the value of the silver ounce, the more commerce it will be able to sustain. In a world in which the values of national and regional fiat currencies are coming under an increasing cloud of doubt, the monetized silver ounce will prove its value as an international currency.

We think that the prestige of London as a financial centre can only be enhanced by this system of “Conditioned Mint” for silver. The silver coin, monetized in British pounds, will prove to be a formidable and worthy competitor for the American dollar and the euro.

We believe that this proposal should be examined as a gradual and non-disruptive means of reintroducing real money into the world’s economy. The latent desire for such money on the part of the world’s population will have found a vehicle for its expression in the monetized silver ounce, and that latent desire will manifest itself through the world market for currencies. Perhaps silver can open the way for an eventual reform of the world’s monetary system based on gold.

The world is waiting for the sunrise

Since ancient times one of the most important activities which any State exclusively reserved to itself was the minting of the nation’s money.

In our age we have seen that modern banking systems have completely usurped this fundamental function of the State. Had the banking systems of the world fulfilled this function correctly, we should not be pondering monetary matters. The fact is that the banking systems of the world have one and all followed the same banking rule book, which they altered when the rules proved an impediment to increased profits, and they have managed to expand themselves into total bankruptcy. Not only that, but having taken over the power of issuing money – of zero quality – they have arrogated unto themselves as if by a natural, God-given right the function of being the central promoters of growth and prosperity.

Thus have the money-lenders promoted themselves into a ruling plutocracy. We are now witnessing the inevitable downfall of these plutocracies which have not been interested in the welfare of their nations, but first, second and last in their own enrichment and power. Thus the plutocrats have bankrupted themselves out of greed and irresponsibility.

We have shown how the Treasury of the UK can have a silver coin minted, and how it can endow that coin with a monetary value. Please notice that we are not assigning this task to the Bank of England. The Bank of England is a Central Bank, a financial institution which regulates banking in the UK.

Among other responsibilities, it is in charge of monetary policy, which means that the creation, maintenance and increase or decrease in the amount of fiat money circulating in the UK is within its authorized sphere of action.

The historic development of banking all over the world has led to the present situation, where all money is the exclusive preserve of banking systems and their Central Banks and where, in fact, there is only one kind of money in the world, fiat money. We live in a world where the dominant paradigm is fiat money issued exclusively by a Central Bank and its related banking system. Humanity today knows of no other money but this! If and when the Treasury of the UK, in obedience to the instructions of Parliament, proceeds to the minting of a oneounce pure silver coin with no engraved value and issues a monetary quote for that coin, this will be a revolutionary event from the point of view of the bankers.

The prevailing paradigm of fiat money, and only fiat money, issued exclusively by the Central Bank and its related banking system will have been broken! The State, through the Treasury, will be creating true money.

This will be permanent money which will remain in circulation until it is so worn out that it has to be replaced, at Treasury expense, with new coinage; money that will never be at risk of disappearing due to a collapse of the banking system. Banking, the business of lending money, is a legitimate business subject to risks which all businesses must run. However, the creation of money is not and cannot be a legitimate function of banking: there is a conflict of interest involved in the union of the two functions. The present worldwide monetary and financial disarray is evident proof of this statement.

The rupture of a paradigm is a rare event; entrenched ideas are hard to dislodge. A fresh approach leads to new avenues of action and opens up new horizons which can resolve the total dead-end confronting the world. The system of fiat money issued by banking systems has exhausted itself and cannot offer real alternatives to progress, but only such aberrations as QE 2.

The first thing that will happen when the prevailing monetary paradigm is broken is that people will immediately begin to regard money in a different light: they will have an option, where there was previously no option at all.

Britain would no doubt receive the monetization of a silver coin most enthusiastically. The demand for the coin would be enormous.

If the bankers are allowed to have their way, there will be no monetized silver coin. They will adamantly oppose it. They will be frightened to death of the preference which the British would surely give to the silver coin. They will allege that if the silver coin becomes a reality, Britain is doomed. The bankers are prisoners of their paradigm and can think in no other terms.

No one can foresee all the consequences of introducing a silver coin into circulation in parallel with paper and digital money. Churchill once said, “In politics, experimentation is revolution.” However, real silver money has been the rule in history, not the exception; thus a partial return to silver money as an option alongside paper and digital money is hardly an innovation or experimentation. In historic terms, what has been experimentation – and QE 2 is avowedly experimentation – has been global fiat money created by bankers who quite evidently have had no notion of what they were doing and did not know or did not care what the consequences of their actions would be. The British would experience the joy of holding real money in their hands and saving money that will surely be worth something in the years to come: money that cannot be devalued. Revolution, for the bankers who have not lived up to the trust placed in them; for the people, it heralds peace of mind and hope for a better future, not revolution.

Should not a proposition which offers something sure to be welcomed unquestioningly by hundreds of millions of individuals all over the world be worth considering, notwithstanding the objections of the bankrupt bankers? The deep-seated dread on the part of the bankers regarding the latent preference for silver (and gold) on the part of the population reveals a fundamental social instability which will have to be addressed at some point.

Politics implies tensions between sets of ideas. At some times, ideas that further social progress, prosperity and good husbandry are paramount; at other times, the prevailing ideas impede prosperity, breed apathy and promote profligacy. There is now a potential tension between two conflicting ideas: the idea of the Welfare State, which is tottering on to its eventual collapse, and the idea of taking one’s welfare back into one’s own hands, which at present revolves around an unexpressed mute desire for savings of real, tangible money such as monetized silver. The monetization of a silver coin would provide a channel for that potential tension and create an enormous tide of savings in silver coins.

We believe that the undoubted desire of all peoples of the West - and of the East, as well - is to enjoy real money as the foundation of their economic efforts, and that this desire has been unexpressed and mute because no one has proposed a means of satisfying it. Silver money, which has ever been the money of the people, can become a reality that comes to life in parallel with the prevailing fiat money. Its further development and growth in importance can be only dimly sketched, but it comes to life pregnant with possibilities.

The creation of a silver coin with a stable monetary value, which can remain in permanent circulation in parallel with paper and digital money, would finally close the circuit that turns a worldwide desire into an actuality. The surge into silver money would be enormous. Should we fear what the people desire, or should we understand that desire and its justification, and open the way for it to express itself?

We also believe that the monetization of a silver coin by the method we have outlined – its various details are suggested but can be altered to suit – can become the irresistible objective of a political party that wishes to come to power; there is a silent desire for real money on the part of all people of the world and - the world is waiting for the sunrise!